The SBTi Net-Zero Standard Is Now Final. What It Means for the Companies That Supply Big Brands.

Version 2.0 moves the framework from ambition to implementation and builds supplier engagement directly into how large companies meet their Scope 3 targets.

From Draft to Final Standard

Earlier this spring, we examined the proposed changes to the Science Based Targets initiative (SBTi) and what they could mean for corporate climate strategies. With the release of the Corporate Net-Zero Standard Version 2.0 on June 11, those proposals are now finalized, giving companies a clearer picture of how climate target-setting and implementation will evolve over the coming years.

The release marks the first major revision to a framework that more than 11,000 companies and financial institutions use to set and validate climate targets. Nearly five years after the original standard was published, Version 2.0 reflects how corporate climate programs have matured and where many organizations have struggled to translate commitments into measurable progress.

For companies that have followed the consultation process, the questions are no longer hypothetical. The framework is final, the transition timeline is established, and the implications are becoming clearer, particularly for suppliers that may assume the changes only apply to large multinational brands.

What Actually Changed

The most significant change is not a single requirement but a shift in philosophy. The original standard focused primarily on target-setting and validation. Version 2.0 places greater emphasis on implementation, reflecting a broader evolution in how climate credibility is assessed.

Several structural changes support that shift. The standard introduces a "best-efforts" framework that recognizes circumstances where companies may fall short of targets despite taking reasonable actions. It provides more flexibility in how organizations set targets across Scopes 1, 2, and 3. It establishes an implementation hierarchy that prioritizes emissions reductions at the source before broader system-level interventions. It also introduces a framework for addressing residual emissions through carbon removals over time.

Each of these changes is important. But for upstream suppliers, the most consequential development is easier to miss.

A Two-Tier System

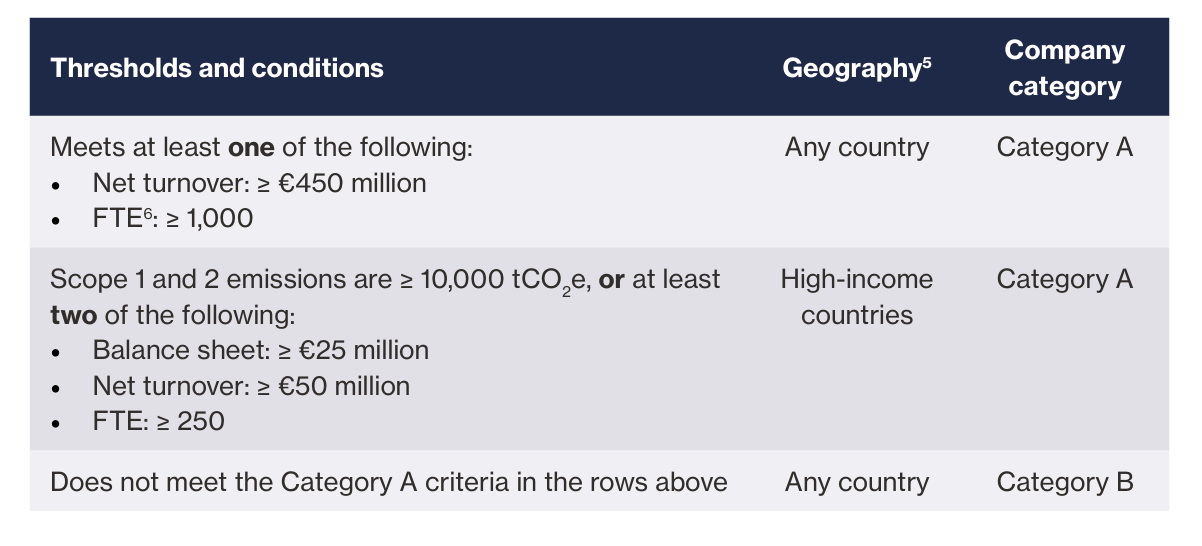

The new version no longer treats all companies the same way.

Category A includes large companies globally, along with medium-sized companies operating in higher-income countries. Category B includes small companies worldwide and medium-sized companies in lower-income countries.

The distinction matters because only Category A companies are required to establish near-term Scope 3 targets, disclose transition plans, and obtain limited assurance over their base-year emissions data. All companies remain responsible for addressing their direct operational emissions through Scope 1 and Scope 2 targets.

For many mid-market manufacturers, that may sound reassuring. If you fall into Category B, the standard places fewer direct obligations on your organization.

That interpretation is technically correct. But it overlooks the way climate expectations move through supply chains.

The Scope 3 Pathway That Reaches You

The companies most likely to fall into Category A are often the same companies that purchase ingredients, materials, components, packaging, and services from mid-market suppliers.

Under Version 2.0, those organizations are required to establish near-term Scope 3 targets. One of the pathways available to them is a supplier and customer alignment approach, where progress is measured by increasing the share of suppliers and customers that have established and are advancing their own science-based targets.

This is the mechanism that turns a Category A requirement into a Category B reality.

As large companies pursue supplier-alignment pathways, their ability to achieve Scope 3 objectives increasingly depends on the progress of their suppliers. What once appeared as customer questionnaires, annual sustainability surveys, or emissions data requests now has a direct connection to how those companies achieve and maintain their own climate commitments.

Whether a supplier falls into Category A or Category B matters far less commercially than whether its customers do.

The standard reinforces this dynamic through its treatment of Scope 3 coverage. Rather than requiring organizations to address every category equally, Version 2.0 allows companies to focus on the emissions sources that are most material and where they have meaningful influence. Suppliers operating within those priority categories are likely to see continued engagement and increasing requests for emissions data, targets, and progress reporting.

SBTi Corporate Net-Zero Standard V2.0 — Company Categorization

Thresholds determining whether a company falls into Category A or Category B.

5 Income classification follows the World Bank country grouping.

6 FTE = full-time equivalent employees.

Source: SBTi Corporate Net-Zero Standard V2.0 (June 2026).

Best Efforts Does Not Mean Lower Expectations

The "best-efforts" provision has attracted significant attention, often because it appears to offer greater flexibility when companies miss their targets.

In reality, it shifts accountability rather than reducing it.

Companies that fall short of a target must demonstrate that they pursued available reduction opportunities, explain the barriers that limited progress, and communicate how they plan to address those challenges moving forward. The emphasis moves from simply achieving a target to showing how an organization is managing toward it.

That reflects a broader trend across sustainability reporting and climate disclosure. Credibility is increasingly tied not only to the existence of a commitment but also to the quality of the evidence supporting progress, setbacks, decisions, and corrective actions.

For suppliers, this matters in two ways. Customers will increasingly seek evidence that demonstrates meaningful action across their supply chains. At the same time, suppliers with their own climate commitments will face growing expectations to explain not only where progress has occurred, but why.

What This Means in Practice

The compliance timeline itself is not particularly urgent. Companies can continue submitting targets under the current standard through early 2028, with Version 2.0 becoming mandatory for new submissions beginning February 1, 2028.

The commercial timeline is another matter.

Many large organizations are already building climate strategies that depend on supplier participation. As they refine Scope 3 programs, suppliers that can provide greenhouse gas inventories, reduction plans, product-level emissions data, and progress updates become easier to integrate into customer climate initiatives.

Those that cannot may find themselves facing increasing scrutiny, additional data requests, or competitive disadvantages during procurement and supplier evaluations.

For most mid-market manufacturers, the practical actions remain familiar. Develop a credible greenhouse gas inventory. Understand which customers are likely to face Scope 3 obligations. Establish a reduction target or a clear path toward one. Build the systems necessary to track and communicate progress over time.

The objective is not simply to satisfy a framework requirement. It is to remain a supplier that customers can confidently include in their own climate strategies.

The Question Behind the Update

The finalized standard does not fundamentally change the direction of travel. It formalizes it.

Pressure on suppliers was always going to arrive through customer expectations, procurement requirements, and growing demand for emissions data. Version 2.0 simply gives those expectations a clearer place within the framework itself.

For many suppliers, the question is not whether the new standard technically applies to them.

The question is whether they will be prepared when their largest customers begin counting on the answer.