CSRD Timelines Are Taking Shape. What 2026 Actually Represents.

For many companies, the immediate focus has become practical. When are we required to report? Which wave do we fall into? How do recent delays affect our obligations?

These are reasonable questions, particularly as updates to the timeline have introduced a degree of uncertainty. But as the schedule becomes clearer, a more useful way to interpret CSRD is not as a single reporting event, but as a sequence that is already underway.

The Timeline Is Now More Defined

At a high level, the structure of CSRD reporting is becoming easier to follow, even with recent adjustments.

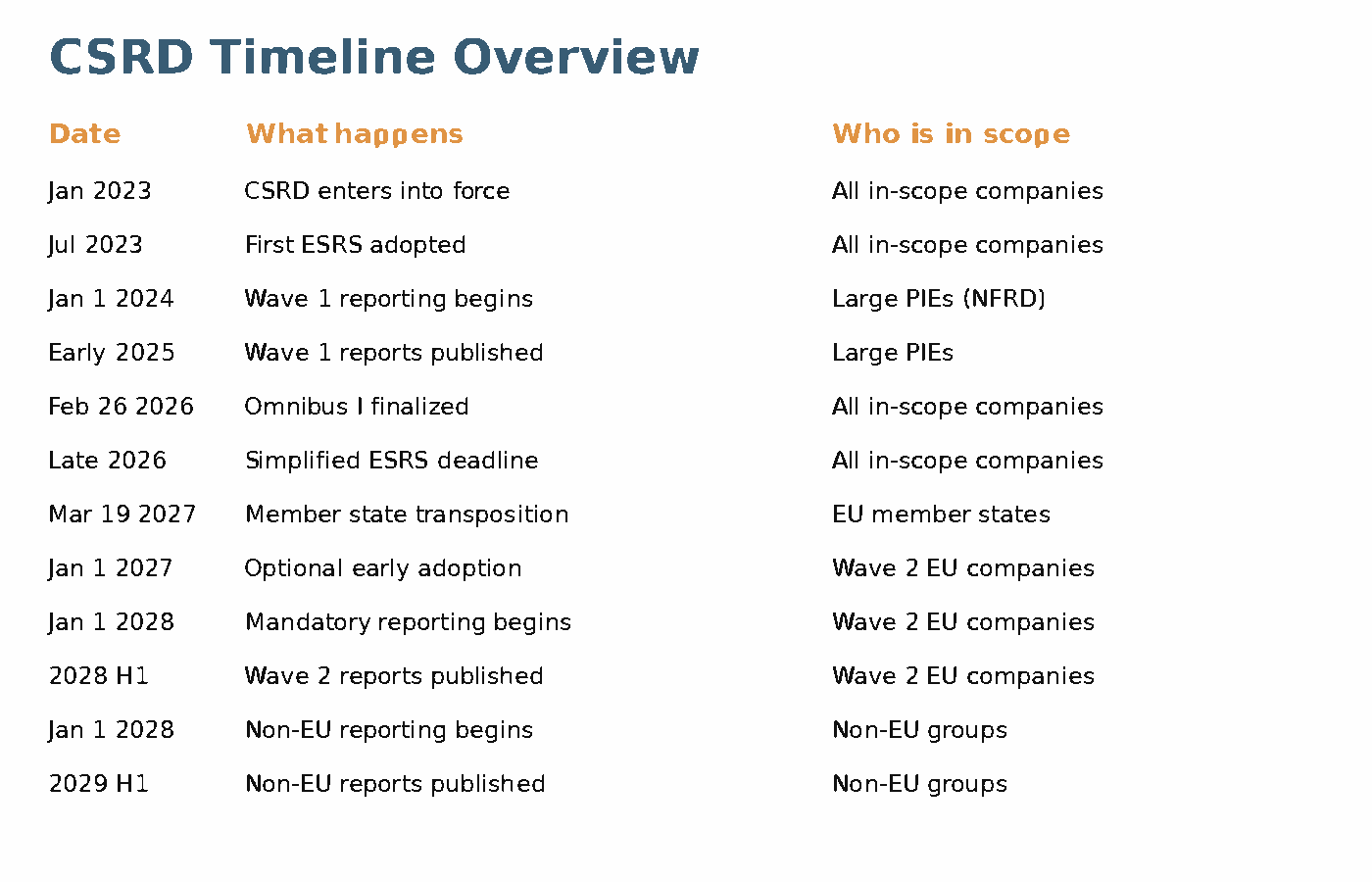

Companies already subject to the Non-Financial Reporting Directive (NFRD) began reporting under CSRD in 2025, based on 2024 data. A second wave of large companies is expected to follow, reporting on 2025 data in 2026, although some of these timelines have been pushed out as part of broader regulatory adjustments.

Beyond that, listed SMEs and non-EU companies fall into later phases, extending into 2027, 2028, and beyond. The result is a staggered rollout, where reporting requirements expand over time rather than applying all at once.

What matters is not just the sequence itself, but how it is playing out in practice.

2026 Sits at the Center

While CSRD spans multiple years, 2026 represents something of a midpoint in the process.

For companies already reporting, it marks a transition from initial disclosure to refinement. The first year of reporting establishes a baseline. The second begins to introduce comparability, consistency, and a clearer understanding of how disclosures will be evaluated.

For companies preparing to report, 2026 is the year where the timeline becomes more immediate. The gap between preparation and disclosure narrows, and the practical realities of aligning data, definitions, and processes become more visible.

For companies not yet in scope, or for those who may never formally report but will still be asked to respond to CSRD-aligned expectations from customers across the value chain, 2026 still has relevance. As reporting expands across industries and regions, expectations begin to move ahead of formal requirements. Requests for information, alignment with frameworks, and exposure to CSRD-style disclosures often arrive before the regulation itself.

In that sense, 2026 is not defined by a single deadline. It reflects a broader shift from anticipation to application.

The Effect of Delays

Recent adjustments to CSRD timelines have understandably drawn attention, particularly for companies in later waves. Delays can change planning assumptions, extend preparation periods, and create space for additional guidance or clarification.

At the same time, they do not fundamentally alter the structure of the rollout.

The sequence remains intact. Large companies report first, followed by additional companies over time, with non-EU entities eventually brought into scope based on their level of activity in the European market.

From a practical standpoint, delays tend to redistribute timing rather than remove requirements. Companies still move through the same progression; the intervals between steps are simply adjusted.

Deadlines Are Becoming More Visible

As the first wave of CSRD reports is published, deadlines are no longer abstract.

They are tied to actual disclosures, which in turn begin to shape expectations across industries. Companies can see how peers are interpreting requirements, how data is being presented, and where differences in approach begin to emerge.

This visibility has a secondary effect.

It shifts the focus from “when do we report?” to “what will reporting look like when we do?” The timeline becomes less about the date itself and more about the level of detail, consistency, and comparability that will be expected at that point.

The Timeline Extends Beyond Reporting Companies

One of the more subtle aspects of CSRD’s phased approach is that its impact does not follow the same timeline for every company.

As reporting companies begin to disclose more detailed sustainability information, they rely on data that often originates outside their direct operations, including suppliers, partners, and other entities that may not yet be formally in scope.

As a result, the CSRD timeline is experienced differently across the value chain. For reporting companies, it is defined by regulatory deadlines. For others, it is shaped by when those disclosures begin to drive requests for data, alignment, and supporting information.

In practice, this means that exposure to CSRD often begins before any formal reporting obligation exists.

What the Timeline Actually Represents

It is easy to view CSRD as a series of deadlines spread across several years.

A more useful interpretation is to see it as a transition that is already in motion.

Each phase of the timeline introduces a new group of reporting companies, but it also builds on the previous one. Early disclosures establish expectations. Later disclosures respond to them. Over time, the system becomes more consistent, more comparable, and more embedded in how companies communicate performance.

From that perspective, 2026 is less about a single reporting requirement and more about the point at which the system begins to take shape in a visible way.

The Bigger Picture

As CSRD continues to roll out, timelines will remain an important reference point. Companies will continue to track deadlines, assess scope, and adjust plans as guidance evolves.

But the significance of those timelines lies in what they represent.

They mark the progression of sustainability reporting from a fragmented set of practices to a more structured and standardized system. They signal when companies enter that system, but not when it begins to affect them.

Because by the time a reporting deadline arrives, the expectations associated with it are already in place.